Roth vs. Traditional 403(b), IRA, and 401(k): What Educators and Retirees Should Know

When people think about retirement savings, the first question is often:

"Am I saving enough?"

That is an important question. But it is not the only one.

Another question can be just as important:

"How will my retirement savings be taxed when I need to use them?"

For educators, public employees, and retirees, that question matters because retirement income often comes from more than one place. Pension benefits, workplace plans, and personal savings may all fit together differently over time. Financial Alternatives is built around helping Washington State clients understand those moving parts with more clarity and confidence.

If you have ever wondered whether Roth or Traditional savings make more sense, this guide will help you understand the difference in plain language.

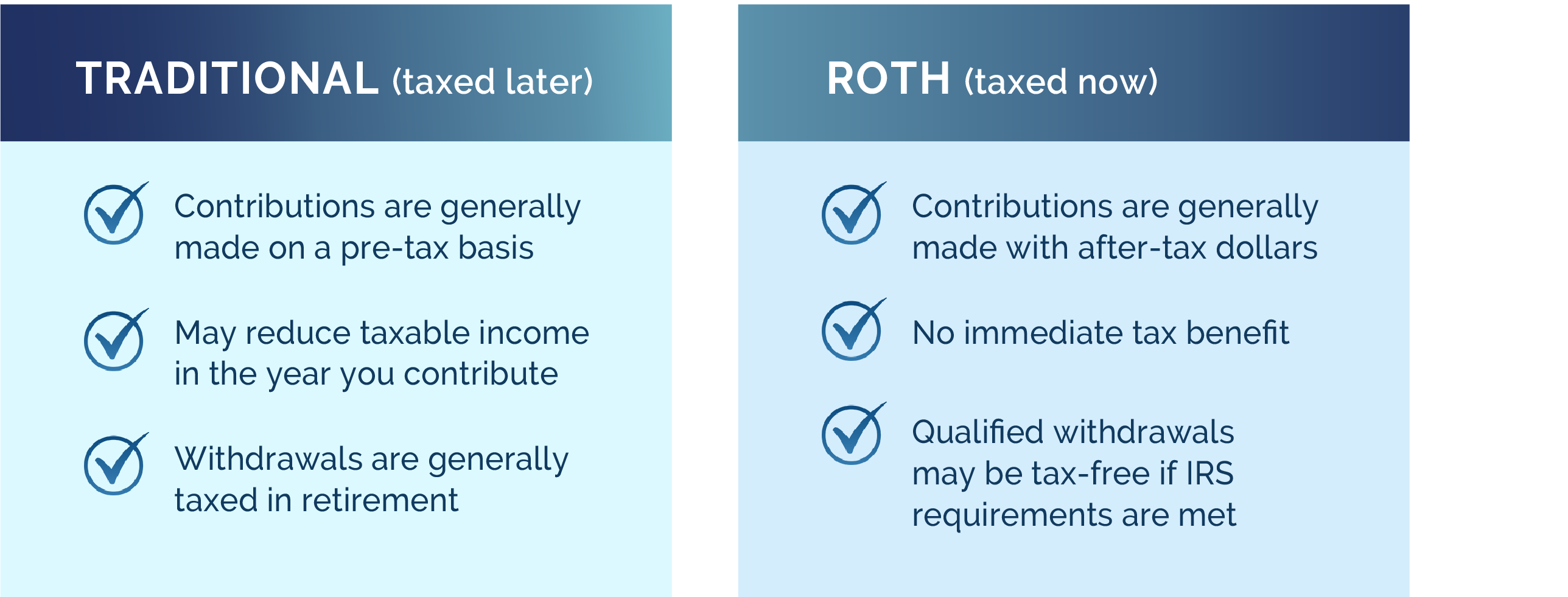

The simple difference between Roth and Traditional savings

At the highest level, Roth and Traditional accounts differ in one main way. The key is understanding how each may fit into your overall financial picture.

That is the core difference. The question is not which type is universally better. The question is how each may fit into your broader retirement picture.

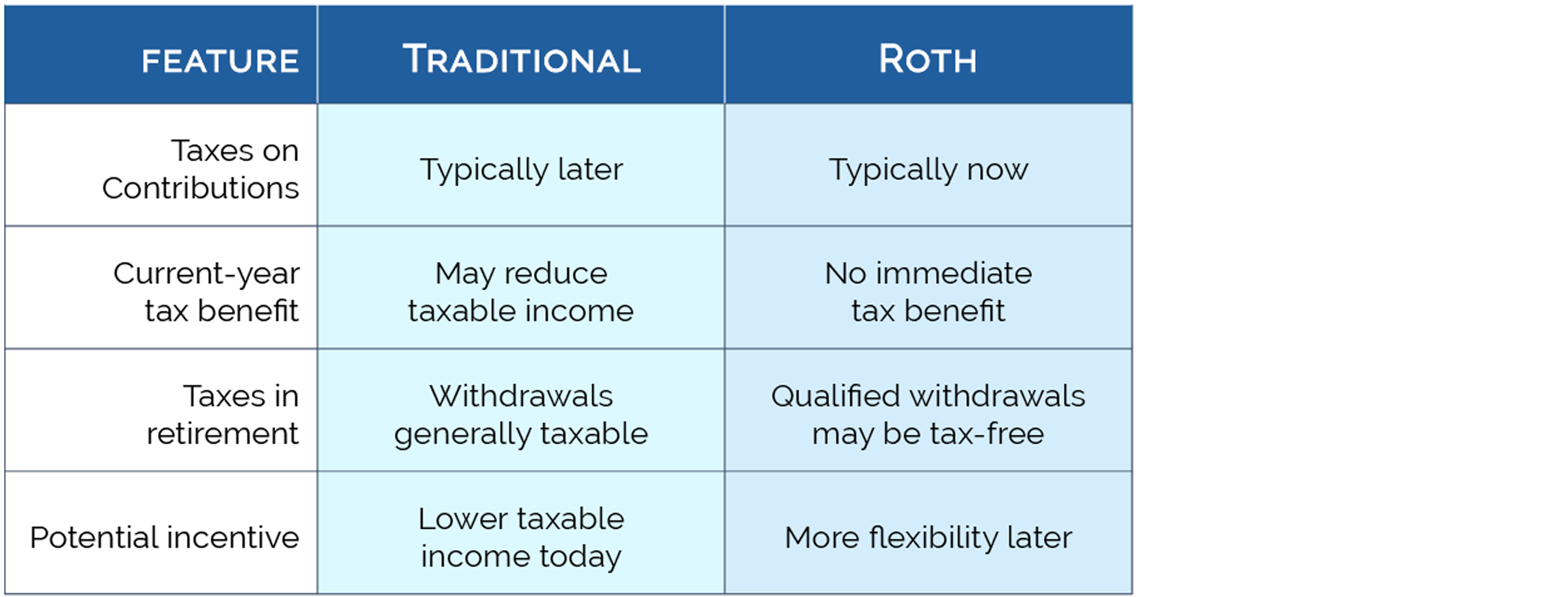

Quick comparison: Roth vs. Traditional

This is a simplified comparison. Specific rules can vary depending on account type, plan design, eligibility, and tax law.

Where you may see Roth and Traditional options

These tax treatments can show up in several different types of retirement accounts.

An IRA is an individual retirement account opened outside of an employer plan. Depending on eligibility, you may use:

• a Traditional IRA

• a Roth IRA

A 401(k) is commonly offered through private-sector employers. Some plans offer only Traditional contributions, while others may offer both Traditional and Roth options.

A 403(b) is common for educators and certain nonprofit or public-sector employees. Depending on the plan, you may be able to contribute on a Traditional basis, a Roth basis, or both.

Some public employees also have access to a 457(b) plan. This can add another layer of retirement planning flexibility, especially when coordinated with a 403(b) or pension strategy.

Not every workplace plan offers the same features. That is one reason it helps to review what your plan actually allows before making assumptions.

Why this matters more for educators and public employees

This is where the conversation becomes more practical.

For many educators and public employees, retirement income may eventually include:

• Pension benefits

• 403(b) or 457(b) withdrawals

• IRA savings

• Roth savings

• Other personal assets

Because those sources may be taxed differently, the type of account you use while saving today can affect how flexible your income feels later.

For example, if most retirement savings are concentrated in pre-tax accounts, more of your income may be taxable when distributions begin. If part of your savings is in Roth accounts, there may be more flexibility in how you think about future withdrawals, depending on your situation and the applicable rules.

That does not mean Roth is automatically the better choice. It means tax diversification may matter.

Why “which bucket” matters in retirement planning

A helpful way to think about this is in terms of tax buckets.

Retirement dollars do not all behave the same way. Where your money is saved can influence:

• Whether you get tax relief today

• Whether distributions may be taxable later

• How much flexibility you may have when planning income

• How different income sources work together

Many people spend years focusing mainly on contribution amounts. That makes sense. But as retirement gets closer, people often realize they also need to understand the tax treatment of those savings.

That is where Roth vs. Traditional becomes less theoretical and more practical.

A simple educator example

Consider a fictional example.

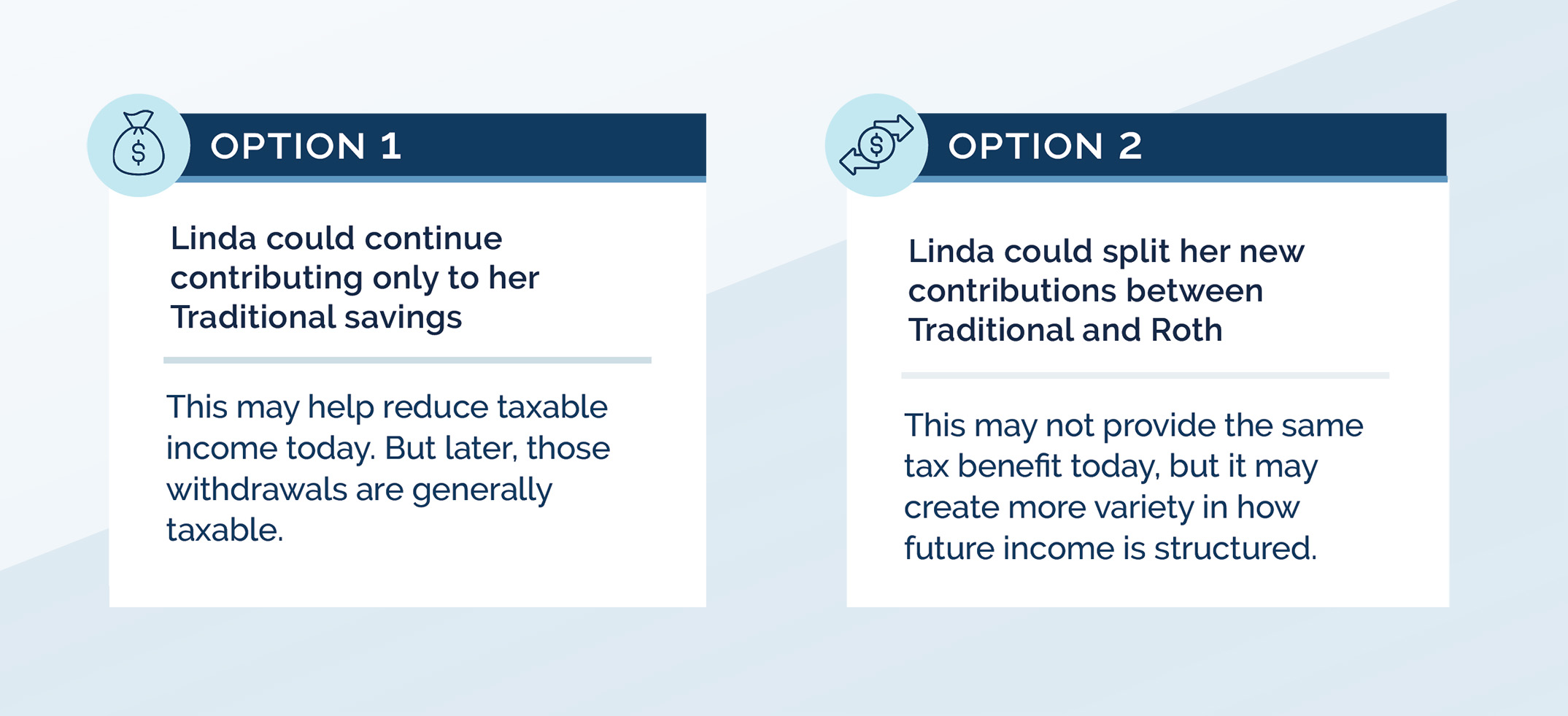

Linda is a Washington State educator in her early 50s. She has been contributing to a Traditional 403(b) for years and expects pension income in retirement. Recently, she has started asking a new question:

"Should all of my new savings keep going into the same pre-tax bucket?"

She looks at two broad options:

The point of this example is not to prove that one approach is right. The point is to show why the decision matters.

For someone with pension income, a long time horizon, and access to multiple account types, the mix of Roth and Traditional savings may deserve a closer look.

When people often revisit this decision

A Roth vs. Traditional review often becomes more relevant when:

- Retirement is getting closer

- Income has changed

- An employer offers a new Roth contribution option

- A household wants more flexibility in future income planning

- Most retirement dollars are concentrated in one type of account

- Pension planning starts to feel more immediate

This is often not a one-time decision. It can be something you revisit as your career, income, and retirement timeline evolve.

Questions to ask before choosing where new savings go

If you are deciding how to direct future contributions, these questions can be helpful:

- What does my current tax picture look like?

- What income sources am I expecting in retirement?

- Am I heavily concentrated in pre-tax savings already?

- Does my 403(b), 401(k), or other plan offer Roth contributions?

- Do I want more flexibility in how retirement income may be drawn later?

- Am I making this decision based on my full picture, or just one account?

These questions do not automatically point to one answer. But they often lead to better conversations and clearer planning.

Common Misunderstandings to Avoid

“Roth is always better”

Not true. Roth can be valuable, but it is not automatically the best fit for every person or every stage of life.

“Traditional is outdated”

Also not true. Traditional contributions may still make sense depending on income, tax considerations, and broader retirement goals.

“If I have a pensions, Roth does not matter”

That is too simplistic. Pension income is one reason some people look more closely at tax diversification, not less.

“All 403(b) plans work the same way”

They do not. Plan features vary, including whether Roth contributions are offered.

“Once I pick one, I’m locked in forever”

Not necessarily. Many people revisit how they direct future savings as their situation changes.

Frequently Asked Questions

"Is a Roth 403(b) better than a Traditional 403(b)?"

Not necessarily. Each has different tax treatment, and the better fit depends on your income, timeline, expected retirement income, and overall planning goals.

"Can I contribute to both a 403(b) and a Roth IRA?"

In many cases, yes, though eligibility and contribution rules apply. It is important to review current IRS guidelines and your personal situation.

Why does pension income matter when comparing Roth and Traditional?

Pension income may affect your tax picture in retirement. That can make the mix of pre-tax and Roth savings more relevant when thinking about flexibility later.

Are Roth withdrawals always tax-free?

Qualified Roth withdrawals may be tax-free if certain requirements are met. The rules can depend on the type of account, timing, and other factors.

Do all employer plans offer Roth options?

No. Some 401(k) and 403(b) plans offer Roth contributions, and some do not.

Bringing it all together

Saving for retirement is important. Understanding how those savings may be taxed can be just as important.

For educators, retirees, and public employees, retirement planning often means coordinating more than one moving part. Pension benefits, workplace plans, and personal savings may all affect the bigger picture.

That is why Roth vs. Traditional is not just an account question. It is really a retirement income planning question.

Financial Alternatives is dedicated to helping our clients think through these decisions with more clarity, especially when educator benefits, retirement systems, and long-term planning all intersect.

Download the Guide

If you would like a shorter, side-by-side version of this topic, download the guide:

Roth vs. Traditional: IRA, 401(k), and 403(b)

It is designed to help you understand the basics in a clear, practical format.

Important Disclosures

The information presented reflects the personal opinions, viewpoints, and analyses of Financial Alternatives and its employees and is developed from sources believed to be providing accurate information. Financial Alternatives or PlanMember Securities Corporation make no representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information presented.

The information presented is not a comprehensive analysis of the topics discussed, is general in nature, is not personalized investment advice and should not be construed as a recommendation to purchase or sell any particular security or strategy. No financial decision should be undertaken without consideration of your personal financial information, investment objectives and risk tolerance with your financial professional. The topics presented may contain information that might assist you in the development of subsequent discussions with the appropriate professionals and should not be construed as individualized advice.

Past Performance does not guarantee future results.

Securities and advisory services offered through PlanMember Securities Corporation, a registered broker/dealer, investment advisor and member FINRA/SIPC. 6267 Carpinteria Ave., Carpinteria, CA 93013 (800) 874-6910. Advisory services also offered through CS Planning Corp., an SEC Registered Investment Advisor. PlanMember Securities Corporation is under separate ownership from any other named entity. Financial Alternatives ©2026 | All rights reserved.